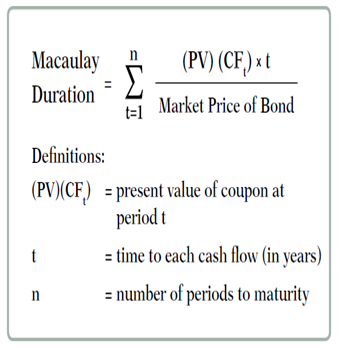

42 duration of a coupon bond

Duration - Definition, Types (Macaulay, Modified, Effective) What is Duration? Duration is one of the fundamental characteristics of a fixed-income security (e.g., a bond) alongside maturity, yield, coupon, and call features. It is a tool used in the assessment of the price volatility of a fixed-income security. Coupon Bond - Investopedia The coupon rate is calculated by taking the sum of all the coupons paid per year and dividing it with the bond's face value. Real-World Example of a Coupon Bond If an investor purchases a $1,000...

Understanding Duration - BlackRock maturity. The higher a bond’s coupon, the shorter its duration, because proportionately more payment is received before final maturity. • Because zero coupon bonds make no coupon payments, a zero coupon bond’s duration will be equal to its maturity. • The longer a bond’s maturity, the longer its duration, because it takes more time

Duration of a coupon bond

Understanding Duration | PIMCO Duration: A measure of the sensitivity of the price of a bond to a change in interest rates. Maturity: The number of years left until a bond repays its principal to investors. Yield: The income return or interest received from a bond. Coupon: The interest payments a bondholder receives until the bond matures. What is the duration of a zero coupon bond? - Quora The duration of a zero coupon bond is equal to its maturity. Duration is a weighted average of the maturities of all the income streams of a bond or a portfolio of bonds. Therefore if there are coupons, the duration will be less than the maturity, and if there are no coupons it will be equal to its maturity. Pete Zeman Coupon Definition - Investopedia Apr 02, 2020 · Coupon: The annual interest rate paid on a bond, expressed as a percentage of the face value.

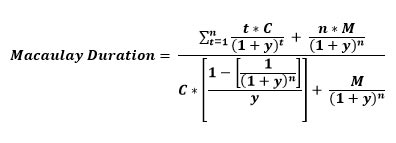

Duration of a coupon bond. How to Calculate Bond Duration - wikiHow Mar 29, 2019 · Bond duration is a measure of how bond prices are affected by changes in interest rates. This can help an investor understand a bond's potential interest rate risk. ... The discount or premium is based upon the bond's coupon rate versus the current interest paid for bonds of similar quality and term. 2. Figure out the payments paid by the bond. What is the duration of a bond? and How to Calculate It? Usually, the duration of a bond shows the number of years in which an investor can recover the present value of the cash flows of a bond. It can also represent a percentage that is a measure of how sensitive the value of the bond is to changes in interest rates. The duration of a bond is simple to understand. › terms › cCoupon Definition - Investopedia Apr 02, 2020 · Coupon: The annual interest rate paid on a bond, expressed as a percentage of the face value. Duration Formula (Definition, Excel Examples) | Calculate Duration of Bond Duration = 63 years; The calculation for Coupon Rate of 4%. Coupon payment = 4% * $100,000 = $4,000. The denominator or the price of the bond Price Of The Bond The bond pricing formula calculates the present value of the probable future cash flows, which include coupon payments and the par value, which is the redemption amount at maturity. The yield to maturity (YTM) …

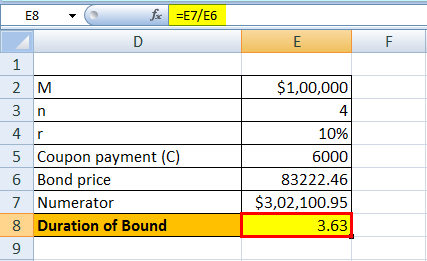

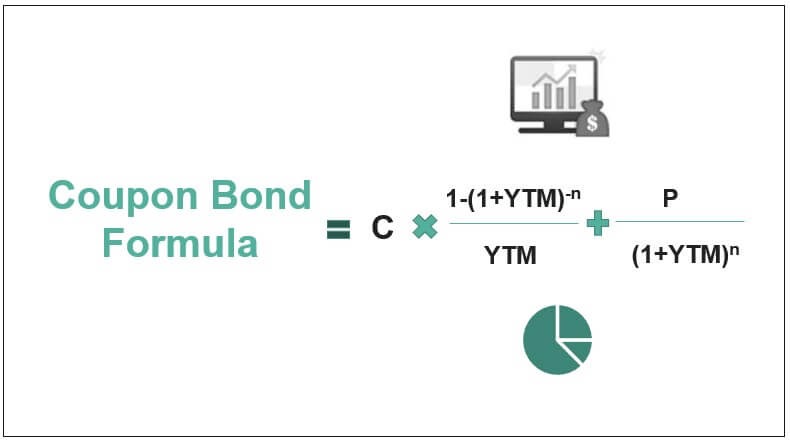

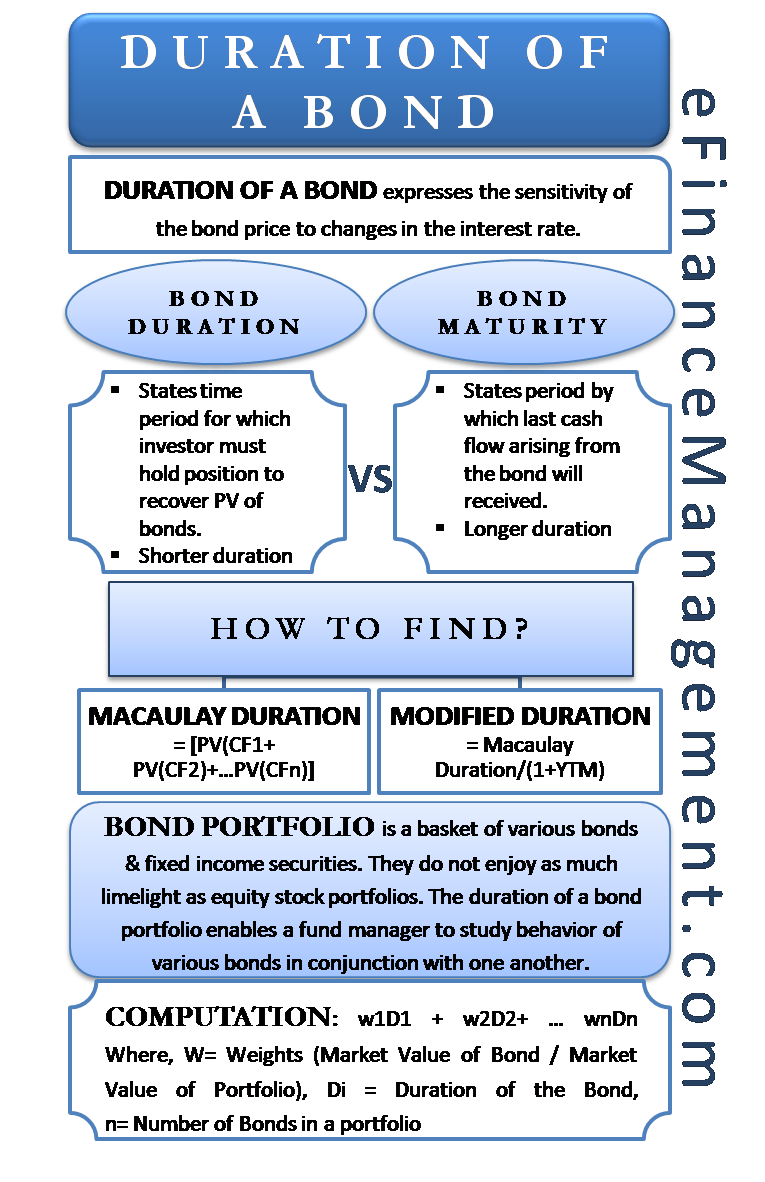

Understanding the Relationship Between Coupon Rates and Duration A high coupon rate bond provides more cash flow than a low coupon rate bond. Accordingly, a high coupon rate bond has a lower duration that a low coupon bond. For example, if I purchase a zero-coupon bond on its issue date the bond will have a duration of 30 years - no cash flow until the bond matures. Bond duration - Wikipedia For example, a standard ten-year coupon bond will have a Macaulay duration of somewhat but not dramatically less than 10 years and from this, we can infer that the modified duration (price sensitivity) will also be somewhat but not dramatically less than 10%. Bond Duration Calculator [Guide 2022]- Nerd Counter A bond duration calculator is used for a purpose that communicates the value change in the worth of security because of an adjustment of financing costs. The idea is that bond prices and loan prices move inversely. This equation is utilized to decide the impact that a 100-basis point (1%) change in loan fees will have on the cost of a bond. Duration Formula (Definition, Excel Examples) | Calculate Duration of Bond Calculate the bond duration for the following annual coupon rate: (a) 8% (b) 6% (c) 4% Given, M = $100,000 n = 4 r = 10% Calculation for Coupon Rate of 8% Coupon payment (C)= 8% * $100,000 = $8,000 The denominator or the price of the bond is calculated using the formula as, Bond price = 88,196.16

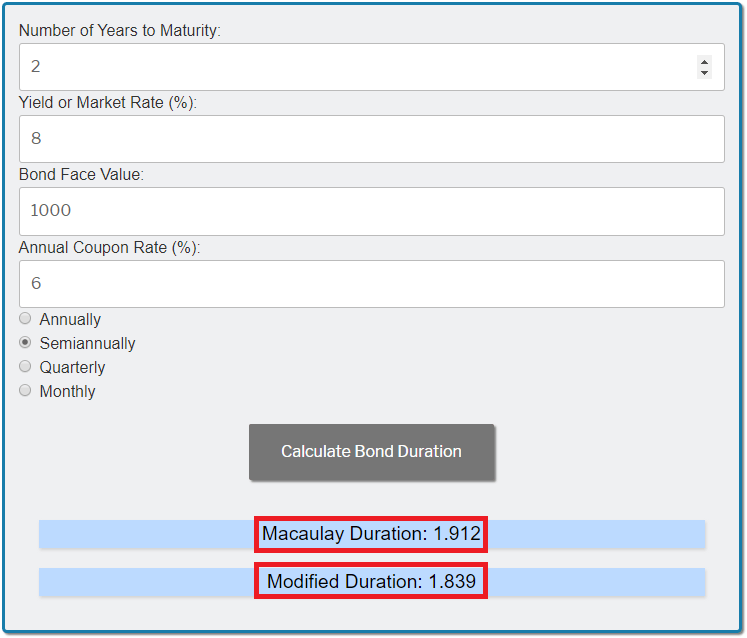

Bond Duration Calculator - Exploring Finance The bond duration calculator can be used to calculate the bond duration. Example is included to demonstrate how to use the calculator. ... Additionally, since the bond matures in 2 years, then for a semiannual bond, you'll have a total of 4 coupon payments (one payment every 6 months), such that: t 1 = 0.5 years; t 2 = 1 years; t 3 = 1.5 years; Understanding Bond Risk | FINRA.org Say you bought a 10-year, $1,000 bond today at a coupon rate of 4 percent, and interest rates rise to 6 percent. ... Duration Risk. If you own bonds or have money in a bond fund, there is a number you should know. It is called duration. Although stated in years, duration is not simply a measure of time. Instead, duration signals how much the ... The Macaulay Duration of a Zero-Coupon Bond in Excel - Investopedia Calculating the Macauley Duration in Excel Assume you hold a two-year zero-coupon bond with a par value of $10,000, a yield of 5%, and you want to calculate the duration in Excel. In columns A and... Bond Duration Calculator – Macaulay and Modified Duration From the series, you can see that a zero coupon bond has a duration equal to it's time to maturity – it only pays out at maturity. Example: Compute the Macaulay Duration for a Bond. Let's compute the Macaulay duration for a bond with the following stats: Par Value: $1000; Coupon: 5%; Current Trading Price: $960.27; Yield to Maturity: 6.5% ...

Duration Analysis

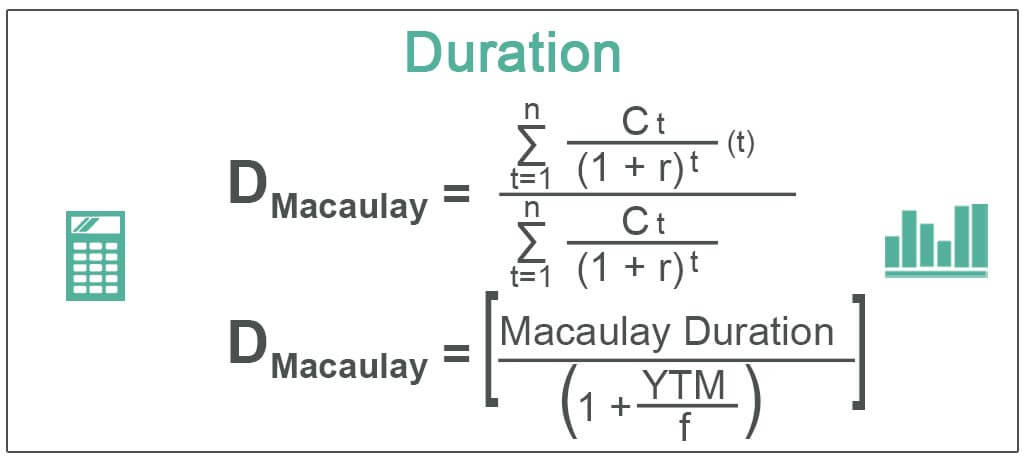

› terms › dWhat Is Duration in Finance? - Investopedia Time to maturity and a bond's coupon rate are two factors that can affect a bond's duration. Macaulay duration estimates how many years it will take for an investor to be repaid the bond's price by...

Duration Formula (Definition, Excel Examples) | Calculate ...

Bond duration - Wikipedia For a standard bond, the Macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero-coupon bond. Modified duration, on the other hand, is a mathematical derivative (rate of change) of price and measures the percentage rate of change of price with respect to yield.

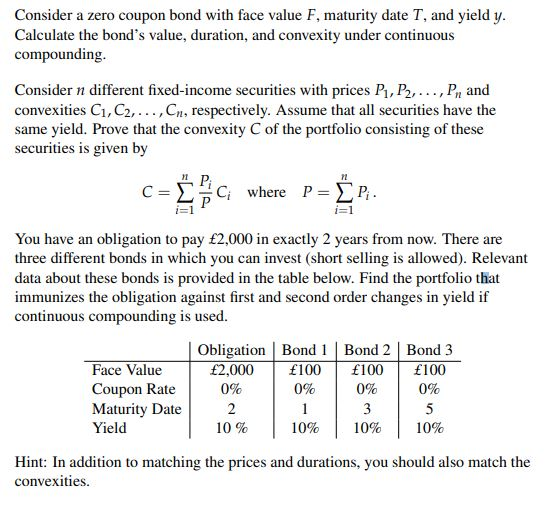

Consider a zero coupon bond with face value F, | Chegg.com

What Is Duration in Finance? - Investopedia Sep 01, 2022 · Duration is a measure of the sensitivity of the price -- the value of principal -- of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years. Bond ...

Making sense of duration sensitivity | Fidelity UAE

Understanding bond duration - Education | BlackRock Conversely, if a bond has a duration of five years and interest rates fall by 1%, the bond's price will increase by approximately 5%. Understanding duration is particularly important for those who are planning on selling their bonds prior to maturity. If you purchase a 10-year bond that yields 4% for $1,000, you will still receive $40 dollars ...

Duration - HowTheMarketWorks

How to Calculate the Bond Duration (example included) PV = Bond price = 963.7 FV = Bond face value = 1000 C = Coupon rate = 6% or 0.06 Additionally, since the bond matures in 2 years, then for semiannual bond you'll have a total of 4 coupon payments (one payment every 6 months), such that: t1 = 0.5 years t2 = 1 years t3 = 1.5 years t4 = tn = 2 years

What Is Duration of a Bond? - TheStreet Definition - TheStreet

› Calculate-Bond-DurationHow to Calculate Bond Duration - wikiHow Mar 29, 2019 · Clarify coupon payment details. To calculate bond duration, you will need to know the number of coupon payments made by the bond. This will depend on the maturity of the bond, which represents the "life" of the bond, between the purchase and maturity (when the face value is paid to the bondholder).

Duration - Definition, Top 3 Types (Macaulay, Modified ...

Zero-coupon bond - Wikipedia Zero coupon bonds have a duration equal to the bond's time to maturity, which makes them sensitive to any changes in the interest rates. Investment banks or dealers may separate coupons from the principal of coupon bonds, which is known as the residue, so that different investors may receive the principal and each of the coupon payments. That ...

Coupon Bond Formula | How to Calculate the Price of Coupon Bond?

› understanding_durationUnderstanding Duration - BlackRock maturity. The higher a bond’s coupon, the shorter its duration, because proportionately more payment is received before final maturity. • Because zero coupon bonds make no coupon payments, a zero coupon bond’s duration will be equal to its maturity. • The longer a bond’s maturity, the longer its duration, because it takes more time

Coupon Bond Duration and Convexity Analysis: A Non-Calculus ...

Duration: Understanding the Relationship Between Bond Prices and ... In the case of a zero-coupon bond, the bond's remaining time to its maturity date is equal to its duration. When a coupon is added to the bond, however, the bond's duration number will always be less than the maturity date. The larger the coupon, the shorter the duration number becomes.

Bond Duration Calculator - Exploring Finance

Coupon Bond - Guide, Examples, How Coupon Bonds Work Let's imagine that Apple Inc. issued a new four-year bond with a face value of $100 and an annual coupon rate of 5% of the bond's face value. In this case, Apple will pay $5 in annual interest to investors for every bond purchased. After four years, on the bond's maturity date, Apple will make its last coupon payment.

Duration of a Bond | Portfolio Duration | Macaulay & Modified ...

Duration and Convexity to Measure Bond Risk - Investopedia Jun 22, 2022 · The duration of a zero-coupon bond equals time to maturity. Holding maturity constant, a bond's duration is lower when the coupon rate is higher, because of the impact of early higher coupon payments.

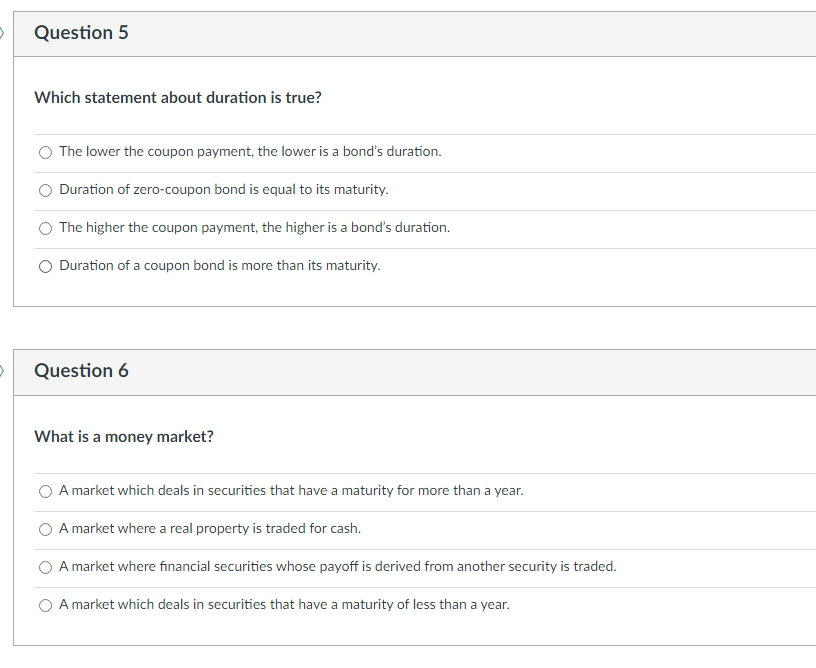

Solved Which statement about duration is true? The lower the ...

dqydj.com › bond-duration-calculatorBond Duration Calculator – Macaulay and Modified Duration Coupon Payment Frequency - How often the bond pays interest per year. Calculator Outputs Yield to Maturity (%): The yield until the bond matures, as computed by the tool. See the yield to maturity calculator for more details. Macaulay Duration (Years) - The weighted average time (in years) for the bond's cash flows to pay out.

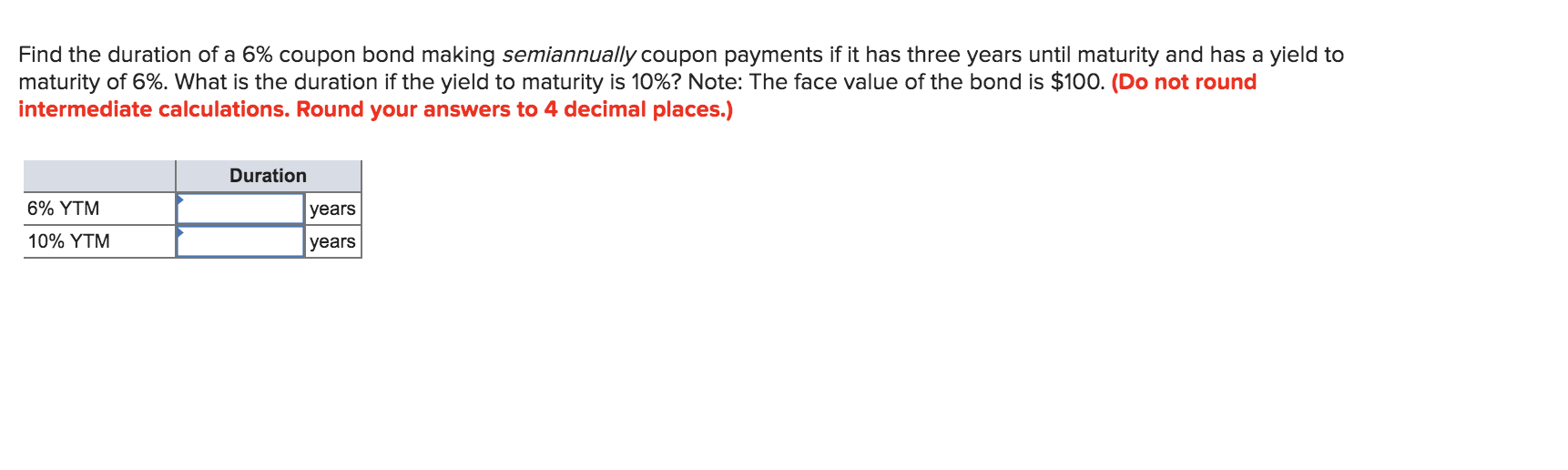

Solved Find the duration of a 6% coupon bond making | Chegg.com

› articles › bondsDuration and Convexity to Measure Bond Risk - Investopedia Jun 22, 2022 · The duration of a zero-coupon bond equals time to maturity. Holding maturity constant, a bond's duration is lower when the coupon rate is higher, because of the impact of early higher coupon payments.

Duration & Convexity - Fixed Income Bond Basics | Raymond James

en.wikipedia.org › wiki › Zero-coupon_bondZero-coupon bond - Wikipedia Zero coupon bonds have a duration equal to the bond's time to maturity, which makes them sensitive to any changes in the interest rates. Investment banks or dealers may separate coupons from the principal of coupon bonds, which is known as the residue, so that different investors may receive the principal and each of the coupon payments. That ...

P1.T3.714. Duration, modified duration and dollar duration ...

Duration | Definition & Examples | InvestingAnswers The lower the coupon, the longer the duration (and volatility). Zero-coupon bonds - which have only one cash flow - have durations equal to their maturities. 2. Maturity. The longer a bond's maturity, the greater its duration and volatility. Duration changes every time a bond makes a coupon payment, shortening as the bond nears maturity.

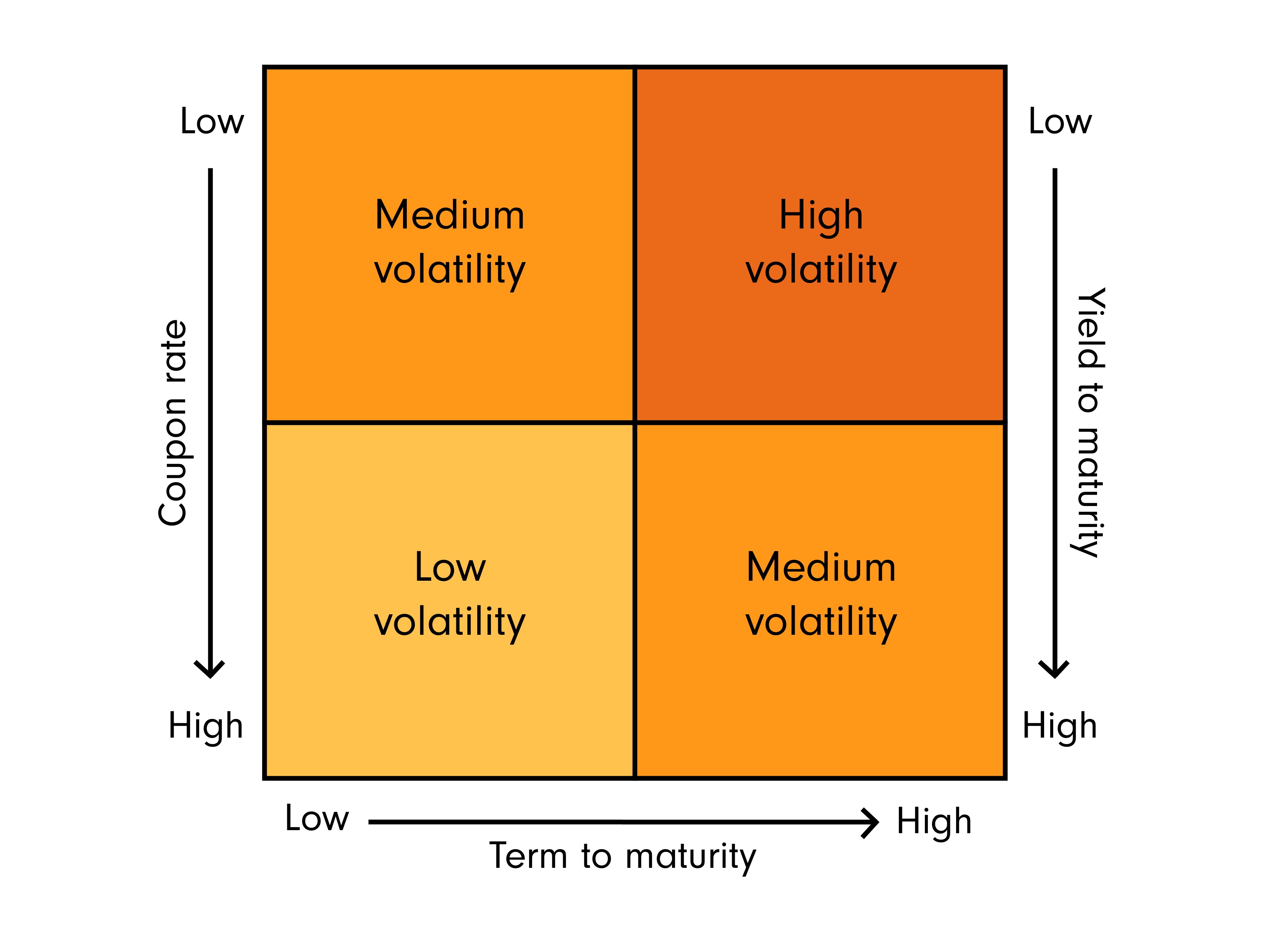

THE RELATIONSHIP BETWEEN YIELD DURATION AND MATURITY

Coupon Definition - Investopedia Apr 02, 2020 · Coupon: The annual interest rate paid on a bond, expressed as a percentage of the face value.

THE DURATION OF A BOND AS A PRICE ELASTICITY AND A FULCRUM

What is the duration of a zero coupon bond? - Quora The duration of a zero coupon bond is equal to its maturity. Duration is a weighted average of the maturities of all the income streams of a bond or a portfolio of bonds. Therefore if there are coupons, the duration will be less than the maturity, and if there are no coupons it will be equal to its maturity. Pete Zeman

Preferred Stocks Live Longer Than Bonds, But Not Always ...

Understanding Duration | PIMCO Duration: A measure of the sensitivity of the price of a bond to a change in interest rates. Maturity: The number of years left until a bond repays its principal to investors. Yield: The income return or interest received from a bond. Coupon: The interest payments a bondholder receives until the bond matures.

Bond Duration | Formula | Excel | Example

Bond's Maturity, Coupon, and Yield Level | CFA Level 1 ...

:max_bytes(150000):strip_icc()/dotdash_Final_Duration_Aug_2020-01-2893c21887d14bb3a81e0a2544fc13c4.jpg)

What Is Duration in Finance?

Zero Coupon Bond - (Definition, Formula, Examples, Calculations)

Solved The duration of a coupon bond is: Multiple Choice Ο ...

Advanced Bond Concepts: Duration | The Financial Engineer

Bond duration - Wikipedia

Giddy/NYU Foundations of Finance Course

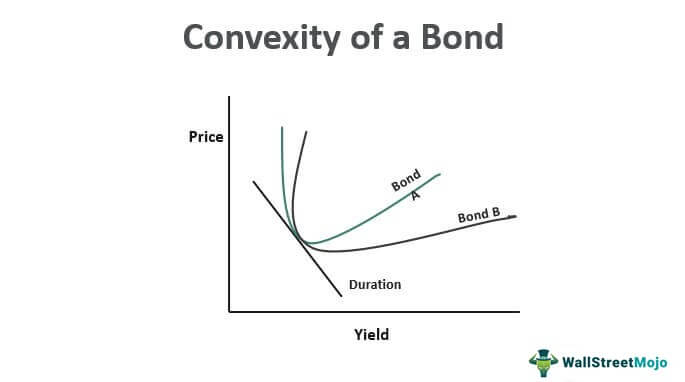

Convexity of a Bond | Formula | Duration | Calculation

Duration and Convexity, with Illustrations and Formulas

WWWFinance - Bond Valuation: Campbell R. Harvey

Interest-Rate Risk II. Duration Rules Rule 1: Zero Coupon ...

Duration: Understanding the Relationship Between Bond Prices ...

Calculation of Duration and Convexity (5-year, $100 face ...

Solved] Calculate the Macaulay duration of an 8 percent ...

Bond Valuation and Risk - ppt video online download

How to use the Excel DURATION function | Exceljet

Class Tutorial Duration & Convexity Solutions - Investment 3A ...

Solved] Find the duration of a 6% coupon bond making annual ...

Bond Price Volatility Zvi Wiener Based on Chapter 4 in ...

FRM: Dollar duration of zero coupon bond

Measures of Price Sensitivity 1

Duration and Convexity, with Illustrations and Formulas

Advanced Bond Concepts: Duration | The Financial Engineer

Post a Comment for "42 duration of a coupon bond"